Namrata Lathi & Boaz Salik

April 2020

10 min read

Data has served different purposes during the COVID pandemic. Here at FischerJordan, we wanted to form a data-driven view of industries disproportionately affected by Covid in the U.S. What could such a view tell us about their stock prices thus far, compared with their near-, medium-, and long-term financial prospects?

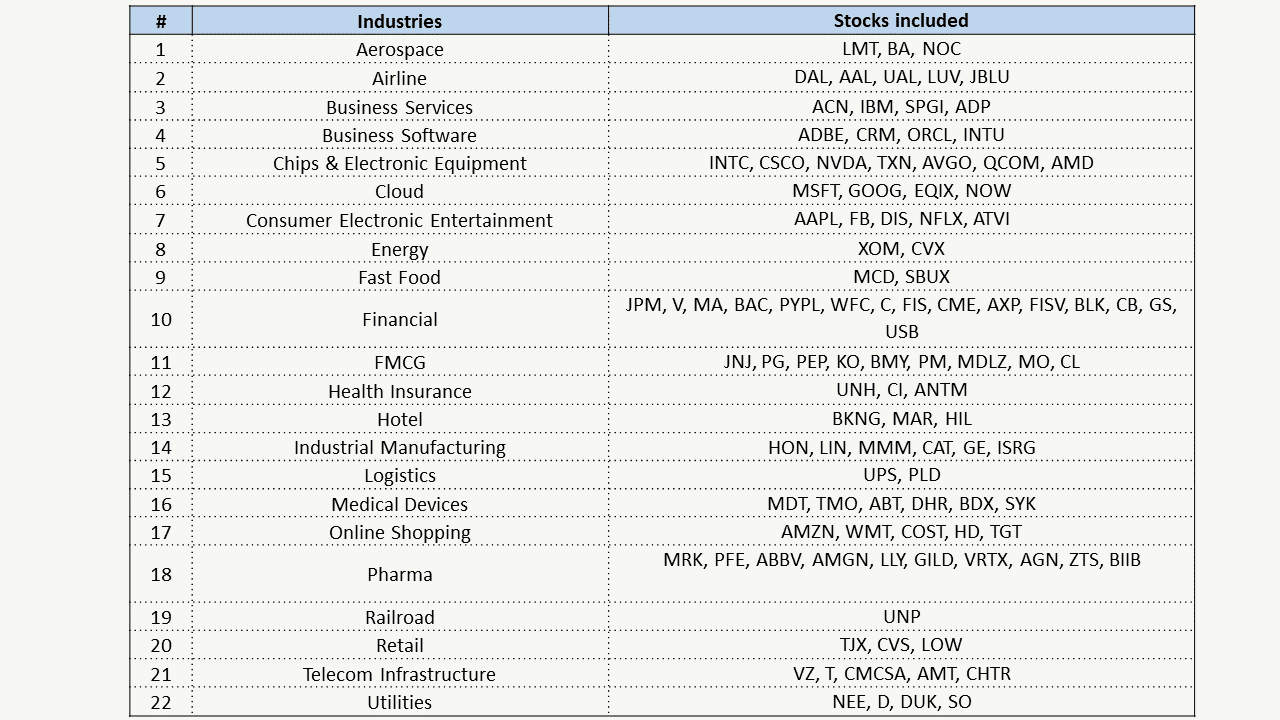

This analysis identifies factors affecting the growth of each industry, starting with 108 of the largest stocks across 22 industries listed on the NYSE and NASDAQ stock exchanges (Fig. 1).

Figure 1 – Industries and included stocks

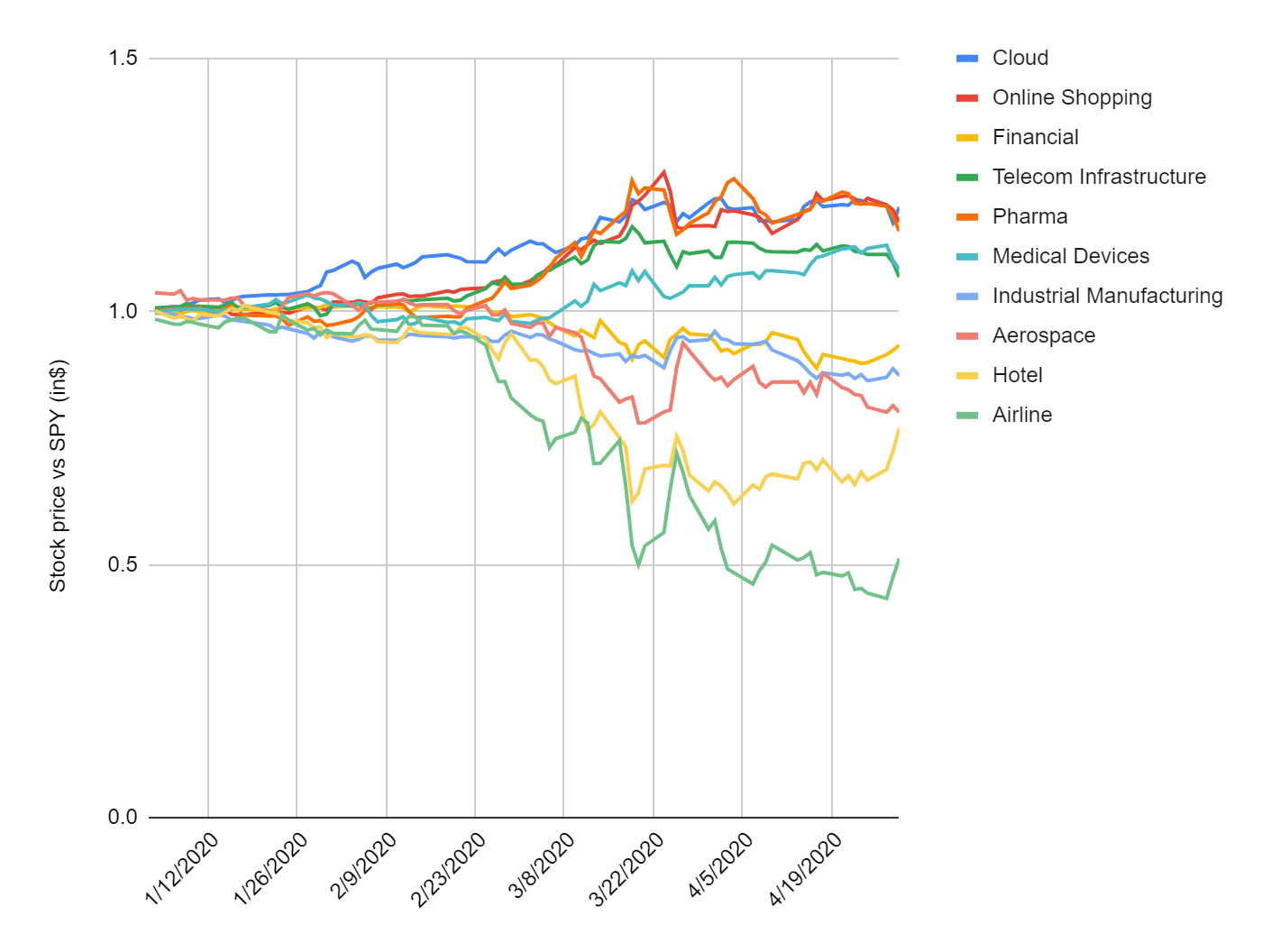

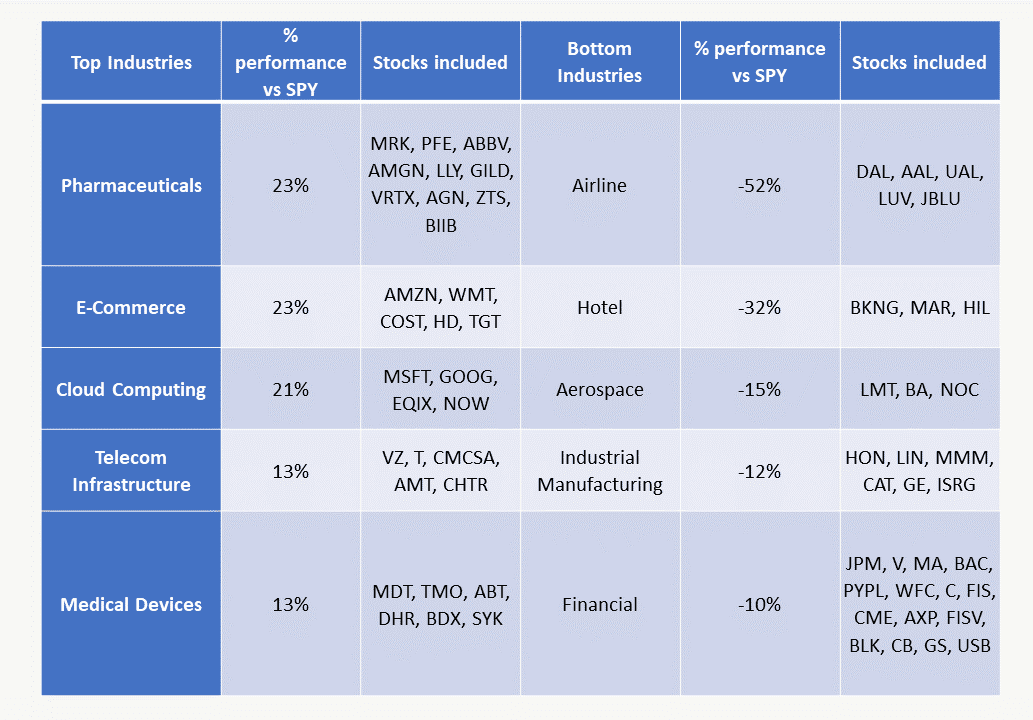

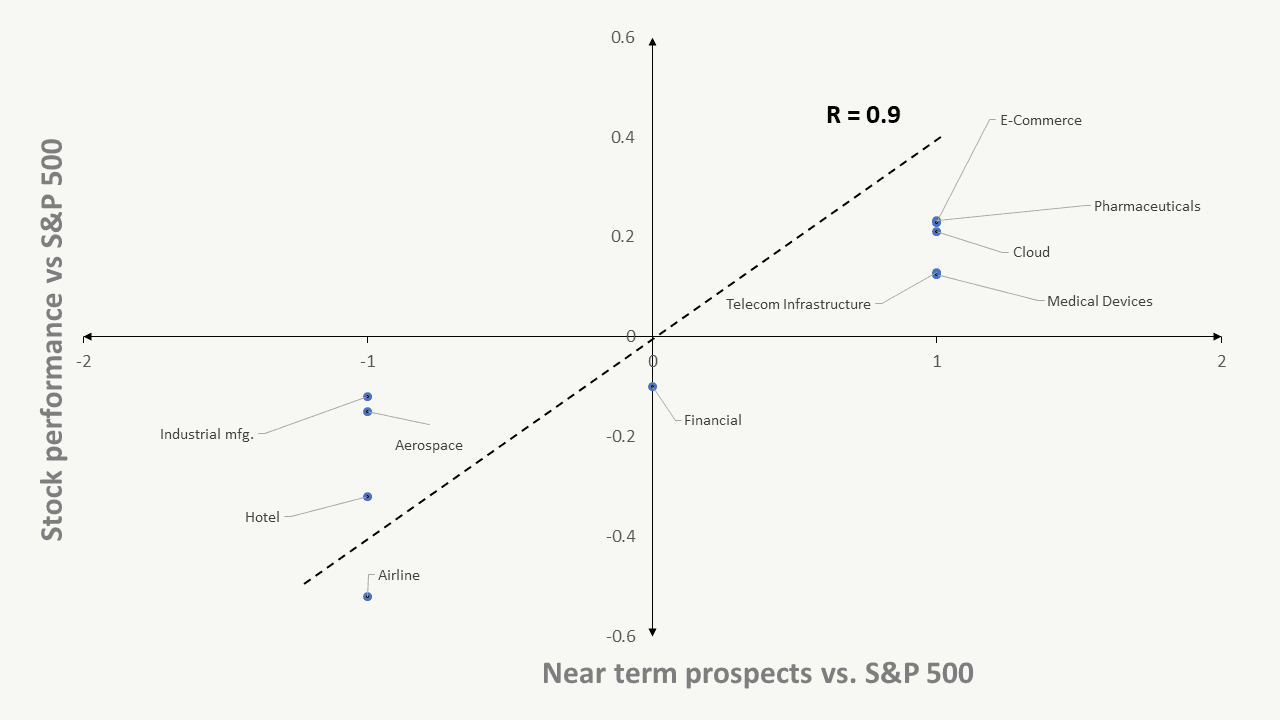

Averaging stock prices within each industry helped us calculate each industry's performance compared to the S&P 500 from January – April 21st 2020 (Fig. 2a) and shortlist the top and bottom five industries. Fig. 2b shows the aggregate performance vs. the S&P 500 since January.

Fig. 2a – Performance of top and bottom industries (from Jan 2020 to Apr 21st 2020)

Figure 2b – Top and bottom industries

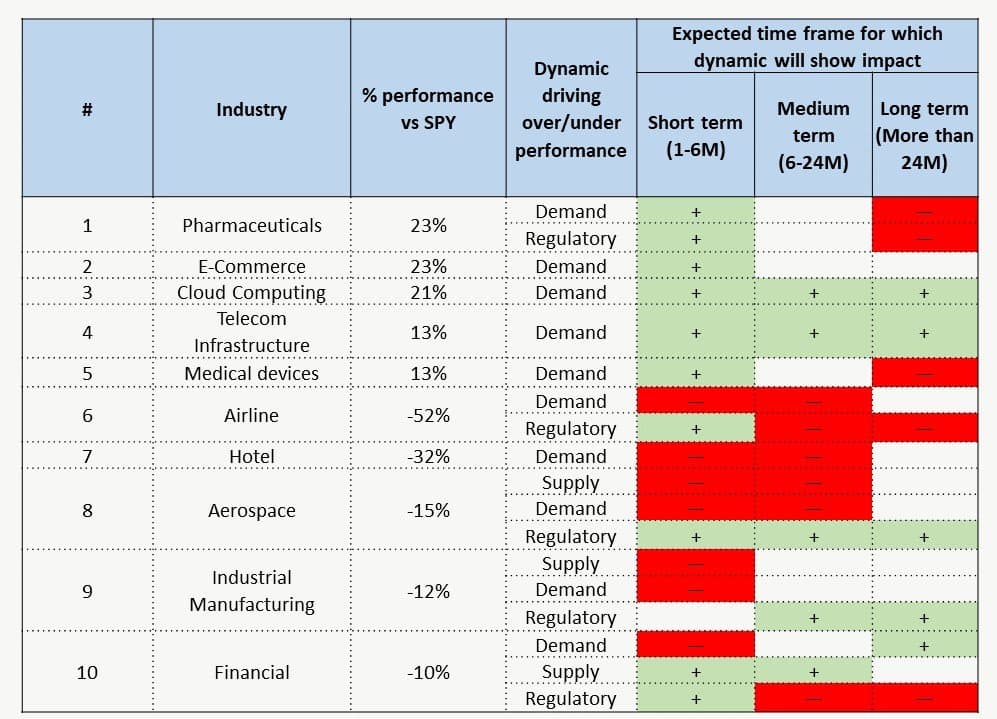

Figure 3 – Dynamics impacting the performance of top and bottom industries

Figure 4a – Expected performance of stocks of top and bottom industries in the near term

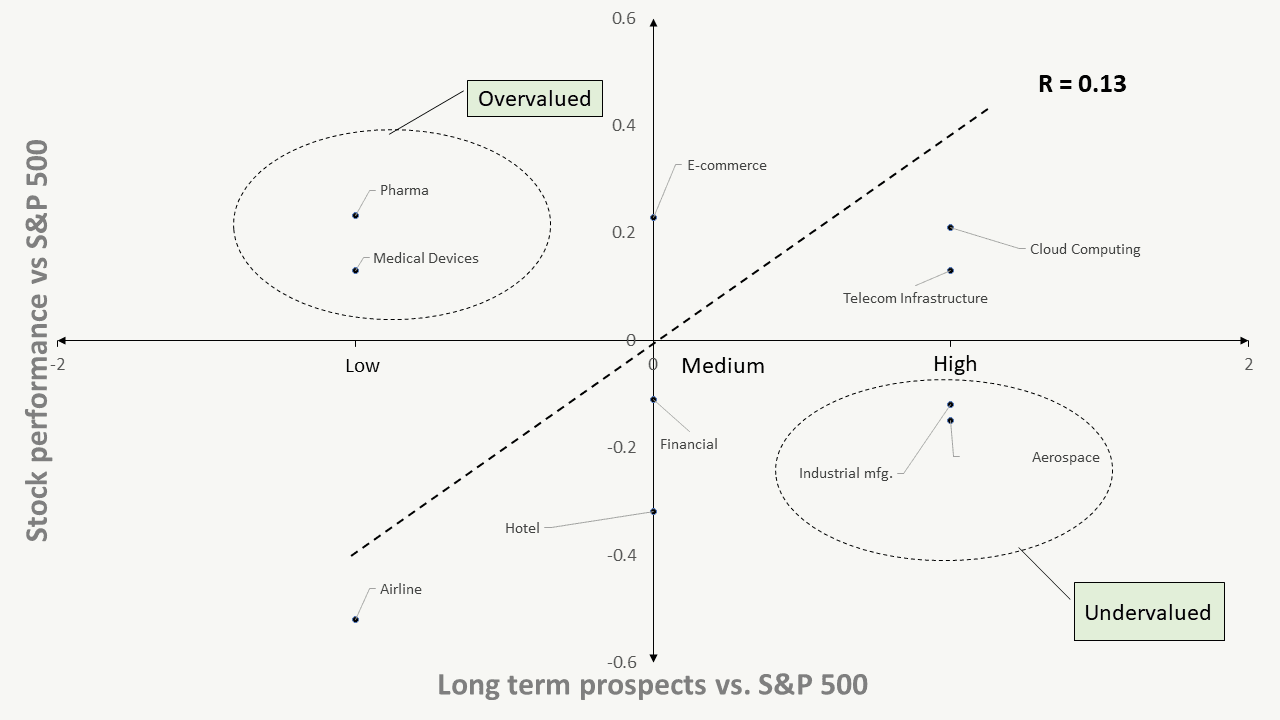

Figure 4b – Expected performance of stocks of top and bottom industries in the long term

This data can inform some assumptions for potential long-term investment opportunities, grouped from overvalued, well-valued, to our up-and-coming undervalued stocks.

Pharmaceuticals — Key drivers: Demand, regulatory. The pandemic has driven a huge increase in demand for vaccines and treatment drugs. Under the CARES Act, the U.S. government has also allocated funds for manufacture of drugs. However, this price spike is likely “short term” to level off as the virus is brought to heel and panic subsides, with the price of Pharma company stocks expected to go down soon. This drop will steepen with advancements in cures or vaccine development. Finally, the reinvigorated possibility of nationalised healthcare represents a long-term decline in these stock prices.

Medical devices — Key driver: Demand. Industries supplying medical devices are facing a substantial – but bifurcated – demand surplus: an increase for medical devices like respirators used to treat coronavirus patients, and a simultaneous decrease for devices used to treat any other diseases. The next six months seem a reasonable timetable for this factor to neutralize. Long-term demand for medical devices may well diminish compared to pre-Covid levels.

Aerospace — Key drivers: Demand, supply. Aerospace firms – currently experiencing a steep decline in overall stock prices – are unique in their prospects for recovery. Supply chain disruptions have impacted production, and decreased demand from airline companies has impacted sales. This will affect firms differently based on their type of manufacturing, however. For those manufacturing passenger jets (most notably BA), continued softness in the airline industry may cause longer-term demand issues, and any government bailout may attenuate longer-term stock performance. For primarily military manufacturers such as NOC and LMT, the potential for escalating tensions between the U.S. and China may lead to greater medium- to long-term demand, making them currently undervalued.

Industrial manufacturing — Key drivers: Demand, supply. Workplace social distancing requirements are impacting supply-side output in manufacturing plants. Meanwhile, slowed economic activity globally tightens demand. But potential government-mandated reduction of imports and a near-term reinvestment in domestic manufacturing may well fuel a price increase for industrial manufacturing shares.

Cloud Computing — Key driver: Demand. The sudden lockdown-induced increase in remote work created skyrocketing demand for services enabling productivity, information access, and virtual communication. Though the future still looks bright for growth in the cloud computing industry, similar sharp increases in the long term seem unlikely without another equivalent demand surge.

E-commerce — Key driver: Demand. A homebound population has reupped demand for online shopping and home deliveries. As restrictions and lockdowns are gradually lifted, this trend will likely slow. Stock prices of e-commerce companies are expected to underperform, but not drastically.

Telecom Infrastructure — Key driver: Demand. The work from home boom has also increased data traffic, with a correlative increase in demand for a sound telecom infrastructure. Companies will likely attempt to increase supply to meet demand, neutralizing the effect of current demand issues and stabilizing stock prices in the medium term.

Airline — Key drivers: Demand, regulatory. The combination of newly safety-conscious, travel-shy consumers and government-imposed travel bans have grounded substantial percentages of global airline fleets. But both these factors are expected to have a medium-term impact on airline stock prices. Government bailouts for these companies will likely avert near-term bankruptcies but may provide a longer-term drag on equity performance.

Hotel — Key driver: Demand. Stock performance for hotel companies is closely tied with the factors influencing airline stocks. Less travel for business and leisure alike diminished demand for hotels, but this is hopefully only a medium-term factor. Highly leveraged hotel companies are unlikely to see much in the form of government bailouts, so their long-term stock prices are expected to remain low.

Financial — Key drivers: Supply, demand, regulatory. Finance industry stocks vary by type of firm. Many larger banks have strong balance sheets despite recent credit loss provisions, but smaller banks and alternative lenders may face stronger liquidity challenges. This combined with the potential for legal headwinds as the ramifications of PPP and other recent loan programs become more clear, make investing in the financial sector difficult at this point, either from the long or short side.

Though the world is still a long ways off from stabilizing in the wake of the pandemic, we can already see some trends developing in these industries most affected by the crisis. Understanding the drivers for the current market dynamics can provide valuable insights for those seeking to make long-term investment decisions at this crucial point in time. We all know the pandemic will end eventually, but not everyone will take the action needed to start planning for it right now. Will you?

Calculated based on stock prices from January 2020 – April 21st, 2020.

Disclaimer

This content is for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on our Site constitutes a solicitation, recommendation, endorsement, or offer by FischerJordan or any third party service provider to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction. All Content on this site is information of a general nature and does not address the circumstances of any particular individual or entity. Nothing in the Site constitutes professional and/or financial advice, nor does any information on the Site constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. FischerJordan is not a fiduciary by virtue of any person's use of or access to the Site or Content. You alone assume the sole responsibility of evaluating the merits and risks associated with the use of any information or other Content on this Site before making any decisions based on such information or other Content. In exchange for using the Site, you agree not to hold FischerJordan, its affiliates or any third party service provider liable for any possible claim for damages arising from any decision you make based on information or other Content made available to you through the Site.

Namrata Lathi & Boaz Salik

Published

April 2020

Reading time

10 min read

Topics

Work with FischerJordan

Our experts are available to discuss how these insights apply to your organization.